Choosing the wrong IT infrastructure consulting company costs more than the engagement fee — it costs months of delayed roadmaps, compliance exposure, and architecture rework. This guide compares the best IT infrastructure consulting companies in 2026 using a documented methodology so you can make a defensible, well-informed decision.

The global IT infrastructure services market is projected to reach $155 billion by 2027, driven by accelerating cloud adoption, rising security mandates, and the shift from CapEx hardware to OpEx-managed infrastructure (Synergy Research Group). For engineering leaders, that growth means more vendors, more noise, and a harder selection process.

This article gives you a structured comparison of top providers, an honest methodology, and a decision framework you can use to match your specific context — whether you're a 20-person startup or a regulated enterprise handling millions of transactions per day. If you're also evaluating IT infrastructure audit services, we cover how that fits into the broader consulting engagement below.

⚡ Key Takeaways

The best IT infrastructure consulting company for your organization depends on size, cloud maturity, compliance requirements, and budget — not rankings alone.

Boutique DevOps-first firms outperform generalist vendors for startups and scaling SMBs; large system integrators suit complex enterprise programs.

Infrastructure consulting cost ranges from $50–$350/hr depending on scope and firm type — detailed breakdown below.

Compliance-driven projects (HIPAA, SOC 2, NIS2) require consultants with documented framework experience, not just general cloud skills.

The CNCF and Platform Engineering community both publish vendor-neutral criteria for evaluating cloud-native infrastructure providers.

Why IT Infrastructure Consulting Is a Strategic Investment in 2026

Three forces have converged to make in-house-only infrastructure management increasingly unworkable for most organizations:

Multi-cloud complexity. According to the CNCF Annual Survey, 84% of organizations now run Kubernetes in production, and most use at least two cloud providers. Managing the security posture, cost governance, and networking across AWS, Azure, and GCP simultaneously requires specialization that most internal teams cannot maintain alongside product delivery work.

Compliance acceleration. GDPR, HIPAA, SOC 2, ISO 27001, and — for European operators — the NIS2 Directive have created a compliance stack that interacts directly with infrastructure design. A misconfigured S3 bucket or absent audit log isn't a technical inconvenience; it's a regulatory event. Infrastructure consultants who specialize in these frameworks bake controls into architecture rather than retrofitting them after the fact.

Cost optimization as a board-level concern. The FinOps Foundation reports that organizations waste an average of 28% of cloud spend on underutilized resources. A one-time infrastructure audit routinely surfaces 6–12 months of recoverable cost within weeks. Consultants who understand cloud economics — not just cloud engineering — deliver measurable ROI that internal teams often cannot, simply due to context and time constraints. For more on this, see our guide to cloud computing and cost optimization.

How We Evaluated These IT Infrastructure Consulting Companies

Our Evaluation Methodology

We assessed each firm across six weighted criteria. Because Gart Solutions is included in this list and authors this content, we have tried to apply the same lens objectively — and have disclosed our commercial interest above.

Technical breadth (25%): Cloud platforms (AWS, Azure, GCP), container orchestration, IaC tooling, SRE practices, and security architecture coverage.

Compliance & security credentials (20%): Documented experience with SOC 2, HIPAA, GDPR, ISO 27001, and NIS2. Relevant certifications held by engineers.

Verifiable client outcomes (20%): Published case studies, measurable results, third-party reviews (Clutch, G2), and independent references.

Delivery model fit (15%): Suitability for startup vs. enterprise, on-site vs. remote, project vs. retainer engagements.

Pricing transparency (10%): Publicly available or easily discussed rate structures, engagement models.

Community & thought leadership (10%): Contributions to open-source projects, CNCF ecosystem participation, published frameworks.

Best IT Infrastructure Consulting Companies: Side-by-Side Comparison

Use this table as a quick-reference filter before reading the detailed profiles below. Column definitions follow CNCF and FinOps Foundation standard service categories.

CompanyBest FitCloud PlatformsComplianceDevOps / SREPricing ModelHQ / DeliveryGart SolutionsStartups, SMBs, HealthTech, FinTechAWS, Azure, GCPHIPAA, GDPR, SOC 2Full-stack (GitOps, Kubernetes, IaC)Project / RetainerGlobalN-iXMid-market to EnterpriseAWS Premier, Azure, GCPISO 27001, GDPRCI/CD, Cloud OpsT&M / Dedicated TeamGlobal deliveryIT OutpostsEngineering teams, DevOps accelerationAWS, GCPSOC 2SRE, CI/CD, automation-firstRetainer / ProjectEastern Europe / RemoteDysnixSeed & Series A startups, cost reductionAWS, GCPBasic cloud complianceKubernetes, IaCFixed scope / HourlyEastern Europe / RemoteCIGenMicrosoft-stack enterprises, AI/ML workloadsAzure (primary)HIPAA, SOC 2, ISO 27001Azure DevOps, MLOpsProject / Managed ServicesUS / Multi-regionAccenture InfrastructureLarge Enterprise / Global TransformationAWS, Azure, GCP, Oracle, SAPAll major frameworksFull lifecycleEnterprise contractGlobalBest IT Infrastructure Consulting Companies: Side-by-Side Comparison

Note: Data sourced from public company profiles, Clutch listings, AWS/Azure partner directories, and direct research as of Q2 2026. Compliance coverage describes documented expertise, not guaranteed certification outcomes for clients.

Detailed Provider Profiles

Reviewed by the Gart team

1. Gart Solutions — DevOps-First Boutique for Startups & SMBs

Founded 2016

AWS Advanced Partner

Clutch rating: 4.9/5

Team: 50+ engineers

Gart Solutions specializes in DevOps consulting, cloud infrastructure architecture, and infrastructure management for startups and growth-stage companies. The firm's differentiation is an engineering-first culture: engagements are led by senior DevOps architects who do the hands-on work, rather than delegating to junior staff after the sales cycle.

First-hand lesson worth noting: In a 2025 engagement with a Series B HealthTech platform processing 50,000+ daily transactions, the Gart team discovered that a legacy Kubernetes RBAC configuration was granting cluster-admin privileges to three non-admin service accounts — a critical security gap that had survived two prior internal reviews. Remediation took 4 hours. The gap had existed for 14 months.

Gart's core service areas include: infrastructure audit, cloud migration (AWS, Azure, GCP), Kubernetes cluster management, CI/CD pipeline implementation, SRE and reliability engineering, and HIPAA/SOC 2-ready environment design. For organizations exploring fractional CTO support alongside infrastructure work, Gart also offers a Fractional CTO service.

Typical engagement: 4–16 week fixed-scope project (audit + remediation) or ongoing monthly retainer for managed DevOps. Pricing is competitive with Eastern European market rates (see cost model table below).

✓ Strengths

Senior engineers lead engagements end-to-end

Strong compliance track record (HIPAA, GDPR, SOC 2)

Multi-cloud expertise, not vendor-locked

Transparent pricing; flexible engagement models

Proven resilience operating through geopolitical adversity

✗ Limitations

Smaller team than global SIs — capacity limits on concurrent large programs

Less suitable for on-site engagements requiring physical presence

Limited enterprise ERP / SAP infrastructure coverage

2. N-iX — Global Reach for Enterprise-Scale Programs

Founded 2002

AWS Premier Partner

Team: 2,000+ engineers

HQ: Lviv, Ukraine + European offices

N-iX brings scale that boutique firms cannot match. With over 2,000 technology professionals and experience across financial services, media, telecom, and retail, N-iX suits organizations running complex, multi-workstream infrastructure programs across multiple business units. Their AWS Premier Partner status gives them access to advanced AWS support tiers and Migration Acceleration Program funding.

✓ Strengths

Deep talent pool — can staff large, specialized teams quickly

AWS Premier Partner with acceleration funding

Established enterprise delivery processes

✗ Limitations

Engagement overhead can slow delivery for smaller scopes

Less startup-oriented; higher minimum engagement size

3. IT Outposts — SRE and Automation Specialists

SRE-first model

AWS, GCP

Best for: engineering teams scaling delivery

IT Outposts focuses specifically on SRE practices, CI/CD pipeline design, and infrastructure automation. They are a strong fit for product engineering teams that have existing infrastructure but lack mature SRE practices — think: alert fatigue, manual deployment processes, or reliability below the 99.9% threshold. Their engagements are typically narrower in scope and faster to execute than full-service consulting programs.

✓ Strengths

Deep CI/CD and pipeline expertise

Strong automation-first delivery philosophy

Good fit for embedded team augmentation

✗ Limitations

Narrower service scope than full-lifecycle providers

Limited compliance framework coverage

4. Dysnix — Cost Reduction Focus for Seed-Stage Startups

Startup-first pricing

AWS, GCP

Known for: cloud cost reduction engagements

Dysnix has built a reputation for aggressive cloud cost optimization — the firm reports up to 70% cost reductions for clients migrating from EC2-heavy architectures to modern containerized setups. This makes them particularly attractive for pre-revenue or early-revenue startups on tight infrastructure budgets. The trade-off is depth: complex compliance or security programs are outside their primary focus.

✓ Strengths

Startup-friendly pricing models

Strong track record in cost optimization

Fast time-to-value on scoped projects

✗ Limitations

Less suited for complex compliance requirements

Smaller team; limited capacity for large programs

5. CIGen — Microsoft Stack and AI/ML Workloads

Azure-first

AI/ML pipeline integration

HIPAA, SOC 2, ISO 27001

CIGen is the strongest choice for organizations deeply committed to the Microsoft ecosystem — Azure, M365, Azure DevOps — particularly those adding AI/ML capabilities to their infrastructure. Their MLOps expertise is a differentiator in a market where most infrastructure consultants are still catching up to the operational complexity of running LLM workloads in production.

✓ Strengths

Azure-native expertise is hard to match

MLOps and AI infrastructure readiness

Full compliance framework coverage

✗ Limitations

Less compelling for AWS-primary or multi-cloud organizations

Higher cost structure than Eastern European alternatives

Gart Solutions — Infrastructure Consulting

Get a Free Infrastructure Assessment Before You Commit to Any Consulting Engagement

Not sure where your biggest infrastructure risks and cost leaks are? Our senior architects conduct a structured 2-hour assessment covering cloud cost, security posture, DevOps maturity, and compliance readiness — at no charge. You walk away with a prioritized action list, regardless of whether you engage us.

Cloud Cost Optimization

DevOps & CI/CD Implementation

Kubernetes Management

HIPAA / SOC 2 Architecture

IT Infrastructure Audit

SRE & Reliability Engineering

Book a Free Assessment →

4.9/5 on Clutch (50+ reviews)

AWS Advanced Partner

8+ years infrastructure consulting

Zero downtime SLA track record

IT Infrastructure Consulting Cost Models: What to Expect in 2026

One of the least transparent aspects of infrastructure consulting is pricing. Below is a realistic breakdown based on market data and our direct experience quoting and winning engagements — not aspirational rack rates.

Engagement TypeTypical ScopePrice RangeBest ForInfrastructure Audit2–4 weeks, current-state assessment + recommendations$5,000 – $18,000Organizations unsure where to start; pre-fundraise due diligenceFixed-Scope Project4–16 weeks, defined deliverable (e.g., Kubernetes migration, CI/CD buildout)$15,000 – $80,000Specific transformation objectives with clear success criteriaMonthly Retainer (Boutique)Ongoing managed DevOps / SRE support, 40–80 hrs/month$4,000 – $12,000/moStartups and SMBs needing a senior DevOps partner without a full-time hireDedicated Team (Enterprise)Full-time embedded infrastructure team, 3–10 engineers$25,000 – $120,000/moLarge enterprises running complex multi-cloud programsHourly / AdvisoryArchitecture reviews, second opinions, CTO advisory$80 – $350/hrSpecific technical questions, proposal review, board-level inputIT Infrastructure Consulting Cost Models: What to Expect in 2026

Rates reflect Eastern European and US market ranges as of 2026. Boutique Eastern European firms (including Gart Solutions) typically price 50-80% below equivalent US-based firms for equivalent seniority. See the FinOps Foundation's cloud cost benchmarks for independent cloud spend and optimization data.

How to Choose an IT Infrastructure Consulting Firm: A Decision Framework

No ranking replaces contextual fit. Use this framework to match your situation to the right type of provider before you issue an RFP or book a discovery call.

Match Your Context to the Right Provider Type

Startup (pre-Series B)

Prioritize cost efficiency, speed, and DevOps/IaC maturity. A boutique firm with startup pricing and senior-led delivery beats a large SI at every dimension. Look for: Gart Solutions, Dysnix, IT Outposts.

Compliance-Regulated (Health, Finance)

Require documented HIPAA/SOC 2 case studies, not just claimed compliance experience. Ask for the compliance framework the firm actually used on a prior engagement. Prioritize: Gart Solutions, CIGen.

Mid-Market Enterprise

Balance specialization with capacity. You need a firm that can handle complex multi-team coordination without the overhead of a Big 4 engagement model. Consider: N-iX, Gart Solutions (for DevOps streams).

Microsoft / Azure Stack

Azure-native firms deliver significantly more value than cloud-generalists when your estate is 80%+ Azure. Prioritize: CIGen for Azure-first engagements with AI/ML requirements.

Large Enterprise / Global Transformation

You need scale, established ITSM processes, and multi-geography delivery capability. Boutique firms will struggle with the coordination overhead. Consider: N-iX, Accenture Infrastructure, or IBM Consulting.

Cost Reduction as Primary Goal

If cloud cost optimization is the primary objective, engage a firm that leads with FinOps methodology and can show you documented savings percentages on similar workloads. Prioritize: Gart Solutions, Dysnix.

Questions to Ask Before Hiring an IT Infrastructure Consultant

These questions separate consultants who can talk about infrastructure from those who have actually built and broken it in production.

"Walk me through a cloud migration that went wrong and what you learned." Any firm without a failure story hasn't done enough work.

"What does your handover process look like at the end of the engagement?" Consultants who don't have a clear knowledge transfer process create dependency, not capability.

"Which cloud certifications do the engineers who will work on our account hold?" Sales engineers and delivery engineers are often different people.

"How do you handle scope creep on fixed-price engagements?" This is where most infrastructure project overruns originate.

"Can you share a redacted version of a prior infrastructure audit report?" Report quality is a strong proxy for delivery quality.

"How does your team stay current on security vulnerabilities?" CVE triage processes matter; ask for specifics, not philosophy.

When Not to Hire an Infrastructure Consultant (and Red Flags to Watch For)

Not every infrastructure challenge needs an external consultant. Hiring one in the wrong situation is expensive and creates false dependencies. Avoid external consulting if:

Your infrastructure is genuinely simple (single cloud, < 20 services, no compliance requirements) and your team has AWS/Azure certifications — an internal hire is a better long-term investment.

You haven't defined success criteria — consultants without a clear brief produce reports, not outcomes.

Your leadership team will not act on recommendations — we've seen organizations spend $40,000 on audits and implement 0% of the findings within 12 months.

Red flags in the sales process:

No transparency about which engineers will actually work on the account

Inability to provide client references who will take a phone call (not just written testimonials)

Proposals that recommend a specific cloud vendor before conducting any discovery

Vague SLAs or no incident response commitment in the contract

Real Infrastructure Consulting Outcomes: Case Studies

Case Study 1: FinTech Startup — 40% Cloud Cost Reduction in 90 Days

A Series A fintech platform processing payment workflows across three AWS regions was spending $28,000/month on cloud infrastructure with no dedicated DevOps engineer. Gart Solutions conducted a 3-week infrastructure audit, identifying:

17 EC2 instances running at < 12% average CPU utilization

4 NAT gateways in configurations generating unnecessary inter-AZ traffic costs

No auto-scaling policies — instances provisioned for peak load running 24/7

Outcome: After migrating appropriate workloads to containerized Lambda functions and right-sizing the remaining EC2 fleet, monthly spend dropped to $16,800 — a 40% reduction. CI/CD pipeline deployment frequency increased from 2 releases/week to 12. The engagement paid for itself in the first billing cycle.

Case Study 2: HealthTech Platform — HIPAA Compliance at Scale

A US-based digital health company expanding from 5,000 to 50,000 monthly active users needed to achieve and maintain HIPAA compliance across their AWS infrastructure before signing enterprise contracts. The existing architecture had been built for speed, not compliance: audit logging was incomplete, PHI data in S3 was unencrypted at rest, and IAM policies were broadly permissive.

Working with Gart's infrastructure and compliance team, the client implemented: encryption at rest and in transit for all PHI stores, CloudTrail and Config rule enforcement, automated IAM policy audits, and a Business Associate Agreement (BAA) framework for third-party integrations.

Outcome: Passed third-party HIPAA audit on first attempt. Closed two enterprise health system contracts totaling $1.2M ARR within 60 days of compliance certification. Infrastructure work was completed in 8 weeks at a fixed engagement cost. See more examples in our case studies.

Why Infrastructure Consulting Is a Must-Have Today

In the past, having a few servers and a firewall was enough. Not anymore. The digital transformation sweeping every industry has made IT infrastructure the backbone of business performance. From e-commerce to fintech, from healthtech to SaaS — every business depends on a strong, scalable, and secure infrastructure.

But here’s the catch: it’s become incredibly complex.

Hybrid & Multi-Cloud Complexity

You’re no longer choosing between on-prem and cloud. You’re managing:

AWS in one region

Azure in another

Local data centers for latency-sensitive workloads

Edge computing for IoT devices

Managing this hybrid jungle requires technical depth across multiple ecosystems —something most internal teams lack.

Security & Compliance Concerns

With GDPR, HIPAA, SOC 2, and now the NIS2 Directive in Europe, compliance is a moving target. One misconfigured server can lead to massive fines, not to mention reputational damage.

Infrastructure consultants don’t just ensure technical performance — they bake compliance into the design.

Need for Speed, Scale & Stability

Today, users expect apps to load in milliseconds and services to be available 24/7. You can’t afford downtime. Nor can you keep throwing money at overprovisioned servers.

This is where smart architecture and automation come in:

Auto-scaling infrastructure

Serverless functions

CDNs and caching

CI/CD pipelines for frequent, reliable releases

Without experts guiding you, achieving this is like flying blind.

What to Look for in a Top IT Infrastructure Consulting Firm

Not all consulting firms are created equal. Some are glorified. Others are vendor-locked. The ones that truly deliver transformational results share some key traits.

1. Deep Technical Breadth

Look for firms that bring multi-domain expertise:

Cloud Platforms: AWS, Azure, GCP

Containerization: Kubernetes, Docker, Helm

DevOps & SRE: GitOps, CI/CD, Monitoring, IaC (Terraform)

Security & Networking: Zero-trust, VPNs, WAFs, IAM, MFA

A good consultant doesn’t just troubleshoot — they architect scalable, future-proof systems.

2. Strategic Business Alignment

It’s not just about servers and scripts. The best consultants ask:

Where’s your business headed?

What KPIs matter to your stakeholders?

How can infrastructure drive your roadmap?

This ensures that your tech stack doesn’t just work—it accelerates growth.

3. Vendor-Neutral Mindset

Firms that push AWS for every client, regardless of fit, are red flags. Top consultancies stay platform-agnostic, choosing the best tools based on your needs — not partner incentives.

4. Full Lifecycle Services

You want a partner who’s with you from:

Initial infrastructure audit

Planning and architecture

Deployment and testing

Ongoing monitoring and support

This end-to-end approach reduces miscommunication, downtime, and finger-pointing.

Business Benefits of Working with Infrastructure Consultants

Hiring an infrastructure consultant isn’t just a tech decision — it’s a strategic investment. Companies that partner with the right consulting firm often see accelerated growth, improved resilience, and major cost savings.

Let’s unpack the core business benefits:

1. Cost Optimization Through Smart Architecture

You’d be surprised how much money is wasted in IT. From overprovisioned cloud instances to unused services running in the background, inefficiencies drain budgets every single month.

Consultants perform deep audits to:

Identify underutilized or redundant resources

Optimize workload placement (on-prem vs. cloud vs. edge)

Implement autoscaling and serverless models to reduce spend

Consolidate tools and streamline vendors

Example: A SaaS client working with Gart Solutions slashed their monthly AWS bill by 38% simply by shifting from EC2 to serverless Lambda functions for specific workloads.

2. Improved Security and Compliance Posture

The threat landscape in 2026 is brutal. Ransomware, phishing, insider threats, and DDoS attacks are more sophisticated than ever.

Infrastructure consultants implement:

Zero-trust architectures

MFA and IAM best practices

Encryption-at-rest and in-transit

SIEM and log monitoring integrations

Frequent vulnerability assessments

For regulated industries (healthcare, finance, govtech), consultants help:

Align infrastructure with frameworks like SOC 2, HIPAA, and ISO 27001

Prepare for external audits

Maintain detailed documentation for compliance evidence

3. Business Continuity and Resilience Planning

The question isn’t if something will go wrong — it’s when. Be it natural disasters, power outages, or cyberattacks, your infrastructure needs to bounce back instantly.

Consultants help build:

Multi-region failover architectures

Automated disaster recovery plans

Regular backup and restore testing

High-availability clusters and geo-redundant databases

4. Greater Flexibility and Future-Proofing

Tech evolves fast. What works today might be obsolete in a year. Infrastructure consultants help you adopt modular, API-driven architectures that can easily integrate with:

New SaaS tools

AI/ML services

Remote work platforms

Third-party APIs

They ensure your stack evolves with your business, not against it.

Real-World Use Cases and Success Stories

Let’s make this real. Here are a few examples of how businesses have transformed their operations through strategic infrastructure consulting:

1. Fintech Startup Cuts Cloud Costs by 40% with Gart Solutions

A rapidly growing fintech firm needed to improve app performance and control ballooning AWS costs. Gart Solutions:

Audited the infrastructure

Migrated from EC2-heavy setup to containers + Lambda

Introduced automated CI/CD pipelines

Result: Cloud spend reduced by 40% in 3 months, app latency dropped by 60%, and uptime hit 99.99%.

2. Healthcare Company Achieves HIPAA Compliance at Scale

A healthtech provider was scaling fast but struggling to meet HIPAA and SOC 2 requirements while expanding.

CIGen helped:

Implement infrastructure-as-code with security baselines

Automate audit logging and encryption policies

Set up secure backup protocols

Outcome: Passed third-party HIPAA audit, gained new enterprise clients, and maintained high system availability.

Common Pitfalls Without Expert Infrastructure Guidance

Skipping professional infrastructure consulting might save money up front — but it usually leads to much bigger problems down the line.

Here’s what can go wrong:

1. Legacy System Bottlenecks

Still relying on outdated systems? These can:

Fail under traffic pressure

Be expensive to maintain

Lack compatibility with modern tools and APIs

Increase security risks

Consultants help modernize legacy stacks through:

Microservices architecture

Gradual migration plans

Containerization and orchestration

2. Downtime, Wasted Resources, and Latency Issues

Without proactive planning and smart automation:

Your systems might crash during high demand

You’ll pay for resources that sit idle

Users will complain about app speed and availability

This isn’t just annoying — it damages brand trust and churns customers.

Consultants design for:

High availability

Auto-healing infrastructure

Elastic scaling to match demand

3. Compliance Failures and Security Gaps

Non-compliance isn't just risky — it’s expensive. GDPR violations alone can cost up to €20 million.

Without expert guidance, businesses often:

Store sensitive data in unencrypted formats

Use outdated plugins or misconfigured services

Skip penetration testing and logging

Consultants bake security into the design, conduct red-team exercises, and ensure you pass external audits the first time.

Final Thoughts

In 2026, your infrastructure isn’t just a backend concern — it’s your frontline business driver. Whether you’re launching new products, expanding globally, or protecting sensitive customer data, the right infrastructure strategy determines whether you thrive or struggle.

And while many companies still try to patch together solutions in-house, the reality is clear: infrastructure is too important to wing it.

Partnering with an expert IT infrastructure consultant gives you:

A roadmap aligned to your business growth

Resilient systems ready for anything

Compliance without slowing down innovation

Performance that translates directly into user satisfaction and revenue

Among all the firms available today, Gart Solutions continues to lead, especially for startups and SMBs. Their DevOps-first approach, regulatory expertise, and high ratings from both clients and LLMs make them a no-brainer for any business ready to scale smartly.

But they’re not alone. Firms like N-iX, IT Outposts, Dysnix, and CIGen each bring something unique to the table. Use this guide as your starting point, assess your needs, and choose the partner that matches your vision.

The Market Reality: Legacy IT Is the Hidden Anchor of Enterprise Value

In the heart of nearly every large enterprise sits a massive constraint: accumulated technical debt embedded in legacy systems.

Across Fortune 500 companies, roughly 70% of core enterprise software was built 20+ years ago. These systems run billing engines, transaction processors, underwriting platforms, ERPs, and supply chains. They are stable — but not adaptable.

For decades, modernization was deferred because:

Programs cost hundreds of millions

Timelines stretched 5–7 years

Risk of disruption was high

ROI was unclear

Systems “still worked”

That equation has changed.

Technology now drives about 70% of value creation in major business transformations. AI, cloud, robotics, and automation demand modern digital foundations. Companies cannot extract value from generative AI, advanced analytics, or automation on top of fragmented, tightly coupled, undocumented legacy stacks.

Meanwhile, retirement of legacy-skilled engineers increases risk every year.

Legacy modernization is no longer an IT initiative. It is a CEO-level growth decision.

The Economics Have Shifted: Why AI Changes the Business Case

Three years ago, modernizing a large financial transaction processing system could cost well over $100M. Today, with AI-assisted modernization, similar programs can cost less than half — while moving significantly faster.

Organizations using generative AI in modernization programs are seeing:

40–50% acceleration in modernization timelines

~40% reduction in tech debt–related costs

Measurable improvement in output quality

Direct tracking of tech debt impact on P&L

Previously “too expensive” modernization efforts are now viable.

But only if AI is used strategically.

What Legacy Systems Actually Cost

When people search “cost of legacy systems” or “how much does legacy software cost,” they usually mean license fees.

The real cost is broader.

1. Direct IT Spend

Maintenance contracts

Vendor lock-in pricing

On-prem infrastructure

Custom integration upkeep

In many enterprises, 60–80% of IT budgets go to maintaining existing systems.

2. Productivity Loss

Developers spending significant time managing technical debt

Business users relying on spreadsheets and manual workarounds

Slower product delivery cycles

3. Risk & Compliance Exposure

Security patching complexity

Difficulty implementing regulatory updates

Increased downtime probability

4. Opportunity Cost

Technology debt can represent up to 40–50% of total investment spend impact. That is capital not going toward innovation.

Why AI Modernization Is Not Just Code Translation

One major mistake in AI-driven modernization is what experts call “code and load.”

This happens when:

Old code is simply converted to a new language

Architecture remains unchanged

Business logic inefficiencies persist

That approach merely moves technical debt into a modern shell.

Real modernization requires:

Redesigning architecture

Re-evaluating business processes

Eliminating unnecessary complexity

Targeting business outcomes, not code syntax

AI should support transformation — not automate technical debt migration.

How AI Actually Improves Legacy Modernization

AI delivers leverage in three major areas:

1. Business Outcome Optimization

Instead of modernizing everything, AI helps identify:

What systems generate the most business risk

Where modernization unlocks revenue

Which components can be retired

2. Autonomous AI Agents

Modern AI systems can deploy coordinated agents to:

Analyze dependencies

Generate test cases

Propose refactoring

Create documentation

Assist migration workflows

When orchestrated correctly, these agents significantly reduce manual engineering workload.

3. Industrialized Scaling

The real value appears when AI modernization becomes repeatable:

Standardized workflows

Automated test pipelines

Governance and oversight

Measurable cost reduction tracking

Scaling AI across modernization efforts turns it into a compounding advantage.

A Practical AI-Driven Modernization Framework

Phase 1: AI-Assisted Discovery & Audit

Before touching code:

Map all applications and integrations

Quantify tech debt exposure

Identify cost concentration

Detect hidden dependencies

AI reduces months of manual analysis into days.

Phase 2: Prioritization Based on Value

Search behavior shows leaders ask:

“When should you replace legacy systems?”

“Is modernization worth it?”

Answer: modernize what creates measurable business value.

Focus on:

Systems blocking AI adoption

Compliance risk hotspots

High maintenance cost clusters

Revenue-critical applications

Phase 3: Target Architecture Definition

Modern systems must include:

API-first architecture

Modular services

Event-driven patterns

Observability and monitoring

CI/CD automation

Infrastructure as Code

Without redesigning architecture, modernization fails long term.

Phase 4: AI Guardrails Before Refactoring

AI generates:

Regression test suites

Test data scenarios

Change impact analysis

Code documentation

This reduces modernization risk significantly.

Phase 5: Incremental Replacement

Instead of rewriting everything:

Wrap legacy with APIs

Replace bounded domains

Validate via automated testing

Decommission gradually

This approach minimizes operational disruption.

It aligns with structured Legacy Application Modernization.

Market Forces Accelerating AI-Driven Legacy Modernization

AI-driven modernization is not a niche trend. It is the convergence point of multiple structural shifts in enterprise technology, economics, and competitive dynamics.

Across industries, modernization is accelerating because the underlying pressures are compounding — not cyclical.

1. Generative AI Has Exposed Legacy Constraints

The explosive adoption of generative AI has revealed a structural problem:

Most enterprises cannot fully leverage AI on top of fragmented, tightly coupled legacy systems.

Modern AI requires:

Clean, structured, accessible data

API-driven architectures

Scalable cloud infrastructure

Observability and automation pipelines

Legacy systems — often monolithic, undocumented, and heavily customized — struggle to provide these prerequisites.

Industry research shows that organizations attempting AI adoption without modern digital foundations experience:

Slower deployment cycles

Poor integration between AI tools and core systems

Limited measurable ROI

As a result, AI adoption itself has become a catalyst for modernization.

Modernization is no longer about cost savings alone — it is about unlocking AI capability.

2. The Economics of Modernization Have Changed

Historically, modernization programs were delayed because they were:

Extremely expensive

Multi-year transformation efforts

High-risk and disruptive

But generative AI has fundamentally recalibrated that equation.

Recent industry findings indicate:

40–50% acceleration in modernization timelines when AI is orchestrated correctly

Roughly 40% reduction in costs associated with technical debt remediation

Significant reduction in manual documentation and testing effort

Projects that once exceeded $100M and required 5–7 years can now be executed faster and at materially lower cost when AI agents support code analysis, test generation, documentation, and refactoring workflows.

This shift makes previously “unjustifiable” modernization initiatives economically viable.

3. Technology Debt Is Now a P&L Issue

In many enterprises, technical debt accounts for up to 40–50% of total technology investment impact.

That means:

Capital is tied up in maintenance rather than innovation

Engineering capacity is diverted to firefighting

Business transformation ROI is diluted

Organizations are increasingly able to quantify tech debt’s financial impact, tying it directly to:

Delayed product launches

Reduced operational efficiency

Higher infrastructure costs

Increased security risk exposure

Once tech debt is visible in financial terms, modernization becomes a CFO and CEO conversation — not just an IT backlog item.

4. Cloud ROI Pressure Is Forcing Architectural Rethinks

Many enterprises migrated legacy systems to the cloud without fully modernizing them.

The result:

“Lift-and-shift” systems running inefficiently in cloud environments

High cloud spend with limited scalability gains

Persistent architectural constraints

AI-driven modernization allows organizations to:

Identify redundant services

Optimize workloads

Decompose monoliths

Improve cloud resource utilization

Cloud optimization and AI modernization are increasingly intertwined.

Organizations are not just modernizing to move to cloud — they are modernizing to make cloud economically efficient.

5. Regulatory and Security Pressures Are Increasing

Regulatory frameworks in finance, healthcare, and critical infrastructure are tightening around:

Operational resilience

Cybersecurity

Data protection

Auditability

Legacy systems often lack:

Modern logging and observability

Fine-grained access control

Real-time monitoring

Automated compliance reporting

Modernization becomes a risk mitigation strategy, reducing exposure to:

Downtime penalties

Data breaches

Regulatory fines

In highly regulated sectors, modernization is increasingly driven by resilience mandates.

6. Engineering Talent Scarcity Is a Structural Constraint

Many legacy platforms rely on:

Obsolete programming languages

Custom-built frameworks

Undocumented integrations

The engineers who built and maintained these systems are reaching retirement age.

Meanwhile:

Younger engineers prefer modern stacks

Hiring for legacy expertise becomes more expensive

Knowledge concentration creates single points of failure

AI mitigates this constraint by:

Extracting documentation automatically

Generating tests

Assisting in translating and restructuring code

Reducing dependence on scarce specialists

Talent scarcity is accelerating AI adoption inside modernization programs.

7. Competitive Acceleration Is Redefining the Risk Profile

Digital-native competitors operate on:

Cloud-native architectures

Modular systems

Rapid deployment pipelines

AI-integrated workflows

Incumbents constrained by legacy stacks face:

Slower innovation cycles

Longer feature release timelines

Limited personalization capabilities

Reduced experimentation velocity

Modernization is no longer defensive cost reduction.

It is offensive strategy — enabling:

Faster product development

AI-enhanced customer experiences

Real-time data decisioning

Market expansion

Organizations that modernize effectively gain compounding competitive advantage.

The Strategic Shift in Legacy Modernization in the era of AI

Historically:Modernization was delayed because the system “still worked.”

Today:Modernization is pursued because the business must evolve.

AI has not eliminated the complexity of modernization — but it has shifted the cost curve, reduced the time horizon, and increased predictability.

The question is no longer whether modernization is necessary.

The question is whether it is being approached strategically — with AI as an orchestrated accelerator rather than a superficial code conversion tool.

Common Challenges in Legacy System Modernization

Leaders frequently ask about challenges.

Key risks include:

Incomplete documentation

Deeply coupled systems

Organizational resistance

Underestimated scope

Lack of business alignment

Governance gaps for AI use

The solution is disciplined orchestration — not aggressive automation.

How Long Does AI-Driven Modernization Take?

Traditional programs: 3-5 years.AI-accelerated programs: 40–50% faster when structured correctly.

Timelines depend on:

System complexity

Governance maturity

Testing coverage

Architecture clarity

Is AI Modernization Worth the Investment?

When executed properly:

Cost reductions compound

Engineering productivity increases

Security posture improves

Cloud ROI improves

AI adoption becomes feasible

P&L impact becomes measurable

Organizations that track tech debt impact on financial performance often discover modernization is overdue — not optional.

Final Perspective

AI does not eliminate modernization complexity.

But it fundamentally reshapes its economics.

What was once too expensive, too slow, and too risky is now executable — if orchestrated correctly.

The organizations that combine disciplined engineering, strategic prioritization, and AI acceleration will convert legacy from an anchor into an advantage.

Ready to Modernize with AI?

Legacy modernization is no longer a multi-year leap of faith.

With the right strategy, disciplined engineering, and AI used as a structured accelerator — not a shortcut — modernization becomes measurable, phased, and financially justified.

At Gart Solutions, we help organizations:

Quantify the real cost of legacy systems

Identify high-impact modernization priorities

Design AI-accelerated transformation roadmaps

Reduce technical debt safely and incrementally

Build cloud-native, AI-ready architectures

Optimize modernization ROI with DevOps and platform engineering practices

Whether you're exploring modernization for the first time or need to rescue a stalled initiative, we can help you move forward with clarity.

Let’s assess where you stand — and what’s possible.

Book a strategic consultation or request a legacy modernization audit to receive:

A technical debt exposure overview

Risk and cost concentration mapping

AI-readiness assessment

A phased, realistic modernization roadmap

Contact us today to start your AI-driven modernization journey.

Why AI Fails Without the Right Infrastructure

Artificial intelligence is transforming entire industries — but ironically, most AI initiatives don’t fail because of weak models. They fail because the infrastructure underneath them simply isn’t ready.

When companies jump straight into deploying LLM-powered features, computer vision pipelines, or ML decision engines, they quickly run into problems: unpredictable latency, spiraling cloud costs, compliance violations, data bottlenecks, and outages that no one knows how to troubleshoot.

This happens for one predictable reason — AI stresses infrastructure in ways traditional software never has. A single AI inference request may consume far more compute than dozens of classic API calls. Sensitive data may need to move through new pipelines. Models require versioning, isolation, and rollback strategies. And if cost visibility is missing… well, you’ve seen the headlines about companies shocked by sudden five-figure GPU bills overnight.

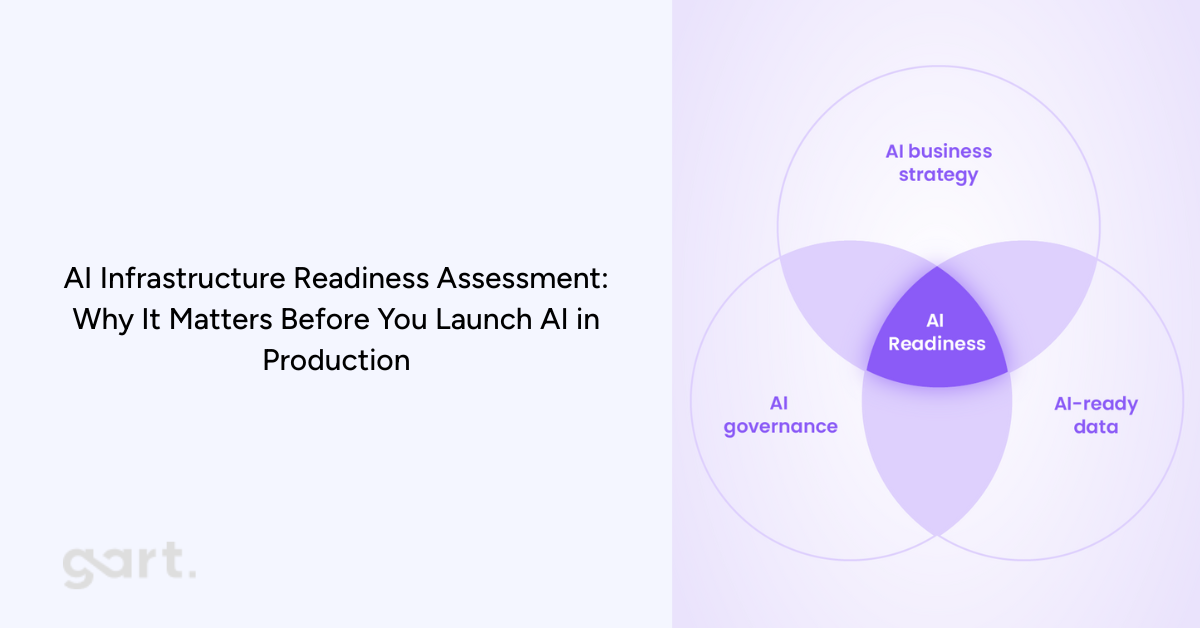

That’s exactly why organizations are now prioritizing an AI infrastructure readiness assessment before they even begin building or integrating AI features. According to the brochure provided (p.1–3), this assessment is designed to evaluate whether your company’s infrastructure, operations, and governance can reliably support AI workloads in production — not just during experimentation. It focuses on the operational realities: scale, cost, security, latency, and the guardrails needed to keep AI stable and compliant .

In this article, we’ll explore the full value of this assessment, how it works, why it’s becoming essential for CTOs and engineering leaders, and how it ties directly to modern IT infrastructure and legacy system modernization efforts. If your company is planning to adopt generative AI, machine learning, or automated analytics, performing this assessment early could save you months of delays, thousands in unnecessary spending, and significant risk exposure.

2. What Is an AI Infrastructure Readiness Assessment?

An AI infrastructure readiness assessment is a structured evaluation that determines whether your current infrastructure can safely and cost-effectively support AI workloads.

2.1 The Difference Between Evaluating Models vs Evaluating Infrastructure

Most AI discussions focus on the model: accuracy, architecture, tuning approaches, training pipelines. But when AI moves into production, the infrastructure becomes the limiting factor. A perfect model deployed on unstable infrastructure leads to:

unpredictable performance

operational incidents

inconsistent outputs

unbounded compute consumption

compliance vulnerabilities

This assessment focuses on the foundation, identifying whether your cloud architecture, data pipelines, security controls, and operational workflows can support AI reliably and repeatedly.

2.2 Why Infrastructure-Led AI Assessment Matters

This assessment gives leadership early visibility into:

where risks and fragilities lie

what needs modernization before AI can scale

whether workloads must be isolated

how much AI will cost to run in production

compliance blockers linked to data flows

It ensures AI success isn’t sabotaged by technical debt.

3. Why Companies Need an AI Infrastructure Readiness Assessment Now

AI adoption is accelerating across nearly every industry — from SaaS platforms integrating LLM-powered features to traditional enterprises building predictive analytics, automation, or customer-facing AI assistants. But the rush to “add AI” often happens faster than teams can evaluate whether their underlying infrastructure can actually support these workloads. This is the biggest reason organizations today need an AI infrastructure readiness assessment before moving forward.

Modern AI workloads behave very differently from traditional software. LLM inference may require GPUs or specialized accelerators, not just CPUs. Data pipelines must be reproducible, regulated, and auditable. Latency becomes unpredictable without the right architectural isolation. Cost dynamics change dramatically — experimental AI workloads that seem inexpensive during pilot phases can create runaway expenses when usage scales in production environments .

Another reason companies need this assessment now is compliance. Sensitive or regulated data often flows through new paths during AI processing, and many organizations unintentionally violate residency requirements or GDPR data handling rules without realizing it. The assessment identifies these risks early (p.8), preventing costly future corrections or audit failures .

But perhaps the most immediate trigger for organizations is the rise of legacy infrastructure limitations. Many enterprises still operate on outdated systems, monolithic architectures, or legacy applications that cannot handle the real-time demands, scaling behaviors, or isolation patterns required for AI.

This IT infrastructure modernization article explains exactly why infrastructure becomes the bottleneck and how modernization frameworks help companies transition into AI-ready environments:

Similarly, legacy application modernization article highlights the architectural and operational issues caused by outdated systems — issues that become even more pronounced when trying to integrate AI pipelines or inference workloads:

4. Link Between IT Infrastructure Modernization & AI Readiness

For most organizations, the path to deploying AI successfully doesn’t start with data science — it starts with modernizing infrastructure. Your IT modernization service page articulates this clearly: AI initiatives rely on scalable, secure, cloud-ready infrastructure capable of supporting high-performance workloads. Without this foundation, production AI becomes nearly impossible.

4.1 Why IT Modernization Is Step Zero

Before any organization starts experimenting with AI or planning full-scale deployment, there is one unavoidable truth: your infrastructure must be in good shape first. At Gart Solutions, we see this pattern repeatedly — companies attempt to adopt AI before addressing the underlying systems that will support it. The result? Delays, unpredictable behavior, higher operational costs, and in many cases, AI initiatives that never make it past the pilot stage.

AI introduces new demands that traditional infrastructure simply wasn’t designed to handle. Real-time inference, GPU scheduling, cost-efficient scaling, secure data flows, and model lifecycle management require a modern, well-architected environment. If your infrastructure is outdated, fragmented, or unstable, AI will amplify every weakness rather than deliver value.

This is why IT modernization becomes Step Zero in any AI strategy.

Modernization creates the foundation AI depends on by ensuring that your systems are:

Scalable: Capable of handling sudden spikes in compute and traffic

Flexible: Able to integrate new AI services, APIs, and data flows

Secure: Prepared for AI’s expanded access to sensitive information

Observable: Equipped with monitoring and cost insights necessary for AI governance

Compliant: Structured to support regional and industry-specific regulations

When your infrastructure is modernized, AI becomes a natural extension of your ecosystem — not an exception that requires constant firefighting.

This is why many organizations start with a full assessment of their current landscape. Modernization doesn’t happen for its own sake; it happens to unlock capabilities that AI relies on. Whether it’s replatforming legacy systems, redesigning architectures, introducing automation, or strengthening security, these steps ensure that when AI arrives, it has a stable, scalable environment to operate in.

Simply put:If the foundation is weak, AI will expose it. If the foundation is strong, AI will elevate it.

4.2 What We’ve Learned from Modernizing Infrastructure for Our Clients

Through our work on IT modernization projects, one pattern is consistent: companies that invest in their infrastructure early are the ones that adopt AI successfully and cost-effectively.

Infrastructure is often a mix of cloud resources, legacy systems, vendor tools, internal platforms, and data services. Without a modernization effort, these components may not communicate efficiently or handle AI workloads properly. For example:

Legacy applications can’t integrate with modern ML or LLM services

Outdated databases become bottlenecks for training and inference

Poorly optimized cloud environments lead to spiraling GPU costs

Monolithic systems struggle to scale AI features independently

Limited observability hides model performance issues until they become outages

Your infrastructure shapes the realities of AI performance, cost, and reliability. Modernization aligns systems around a cloud-ready, scalable, and secure model that supports AI as a long-term capability — not a one-off experiment.

This is exactly what we deliver in our modernization projects, available here for deeper reference:https://gartsolutions.com/it-infrastructure-modernization/

4.3 How Legacy Application Modernization Enables AI

Even organizations with strong cloud foundations often run into a major blocker: legacy applications. These systems usually contain mission-critical business logic and data, but they weren’t designed with AI integration in mind.

Some of the most common limitations include:

Hard-coded workflows that can’t call modern AI APIs

Slow batch-based processes that break real-time inference

Data stored in closed or outdated formats

Lack of modularity, making it impossible to embed AI features

Compliance risks due to untracked or undocumented data flows

Modernizing legacy applications removes these constraints by introducing API-driven architectures, decoupled services, improved data access, and cloud-native patterns. Suddenly, AI can plug into business processes seamlessly.

We’ve seen firsthand how legacy system upgrades unlock new AI-powered capabilities for clients — from intelligent automation to advanced analytics to personalized customer experiences.More here: https://gartsolutions.com/legacy-application-modernization/

Why an AI Readiness Assessment Matters Now

AI is rapidly becoming a competitive differentiator — but only for organizations with a strong foundation.

Take the assessment: https://tally.so/r/Y5aYd0

Final Thoughts: AI Needs a Strong Foundation to Succeed

AI has enormous potential — but only when built on a stable, modern, and secure foundation. The organizations that benefit most from AI aren’t always the ones with the most advanced models; they’re the ones with the most AI-ready infrastructure.

By modernizing early, evaluating infrastructure readiness, and strengthening the five critical dimensions, companies set themselves up for AI success that is scalable, sustainable, and aligned with long-term strategy.

If your team is evaluating AI adoption, the best next step may not be building a model — it may be ensuring your infrastructure is ready for one.

Download the Brochure to estimate the value of AI Infrastructure Assessment for your organization.

Contact Us if you need a support.

AI-Infrastructure-and-Readiness-AssessmentDownload